Article

Singapore’s Individual Accountability Model will Improve Conduct: Live Poll

Risk and compliance practitioners support the Singaporean conduct regulator’s plans to bring in a light-touch, principles-based framework for management accountability, despite tougher laws being introduced elsewhere across the region.

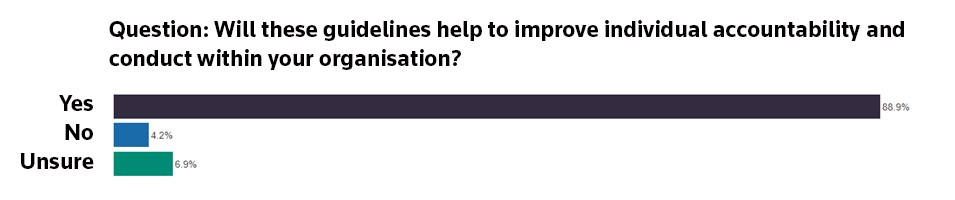

A Thomson Reuters live poll of more than 250 regulatory practitioners in the financial services sector found that 88% believe the Monetary Authority of Singapore’s (MAS) new Individual Accountability and Conduct (IAC) Guidelines will be effective. The guidelines will take effect from September 2021 to promote greater accountability for senior managers, strengthen oversight over people in “material risk” roles and reinforce conduct standards.

Almost nine out of every 10 participants in the live poll said the supervision-based regime would improve accountability and conduct within their organisations and across the Singaporean financial sector.

Nathan Lynch, Thomson Reuters’ Asia-Pacific manager for regulatory intelligence, said financial institutions in Singapore had an opportunity to embrace the “guidelines” and improve conduct standards as an alternative to more intrusive and prescriptive regulation. He said the MAS could move to a statutory regime — such as the frameworks in the UK, Hong Kong and Australia — if the IAC guidelines prove ineffective.

"This is definitely the most light-touch, least prescriptive model across the major financial centres in the Asia-Pacific region so far. The regulatory and political dynamics are quite unique in Singapore, so this is really an opportunity for the industry to get on the front foot and avoid some of the more intrusive regulation we’ve seen in the UK and Australia," Lynch said.

Niall Coburn, regulatory intelligence expert at Thomson Reuters, said the obligations were significant and firms would be sensible to get started with embedding the reforms as quickly as possible.

“This is a significant piece of work,” he said. “MAS makes it clear that the guidelines are not intended to be exhaustive or prescriptive, and that organisations should not adopt a ‘check-box’ mentality in applying them. Instead, the regulator expects financial institutions to identify what enhancements need to be made, based on the nature, size and complexity of their business.”

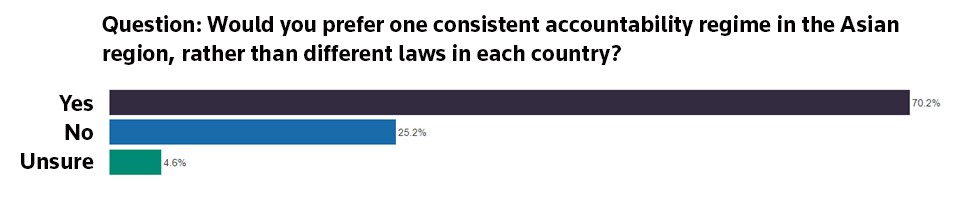

The webinar also heard that regulators across the Asian region should work together to ensure a consistent regional approach is taken to individual accountability. Seven out of 10 respondents said they would prefer to have consistency across the Asian region, rather than dealing with different rules in each country.

“It must be confusing for all the financial institutions that have to deal across the jurisdictions to comply with the regimes and align their business interests as well,” Coburn said.

Supervisory model

The regime in Singapore will be managed through MAS’s existing supervisory and enforcement powers. In Australia, by contrast, the Banking Executive Accountability Regime (BEAR) regime is covered by dedicate legislation and the maximum penalty for breaches is A$210 million.

Kelly-Ann McHugh, Asia-Pacific manager at MyComplianceOffice (MCO), said the guidelines were part of a more proactive enforcement stance at the Singaporean regulator. The MAS has imposed S$11.7 million in civil penalties and secured nine criminal convictions in the past year. These figures were likely to increase in 2021 when the IAC regime takes effect, she said.

“Firms must focus on the key objectives of the guidance and implement best practices for improving the culture in their organisation. Extending fit and proper certifications beyond licensed individuals to senior management is a good example, as well as providing regular training on both bad conduct and good conduct that has been identified internally or within your industry,” McHugh said.

Many organisations will need to re-examine their governance to ensure effective management lines of accountability, especially where they operate in a corporate group or have downstream subsidiaries, the speakers said.

“Governance is essential to ensure the senior managers fulfill their roles and to ensure there is a baseline of integrity and fitness of roles throughout the organisation,” Coburn said.

The guidelines will take effect from September 2021 and are expected to promote greater accountability for senior managers, strengthen oversight over people in “material risk” roles and reinforce conduct standards.

By submitting this form, you acknowledge the Thomson Reuters group of companies will process your personal information as described in our Privacy Statement, which explains how we collect, use, store, and disclose your personal information, the consequences if you do not provide this information, and the way in which you can access and correct your personal information or submit a complaint.